₹10 Lakh Investment Strategy:

Higher returns come with higher risk.

- Can generate strong returns if the fund performs well

- But exposes you to concentration risk

- Spreads risk across categories

- Reduces dependency on a single fund

- Creates smoother return journeys

- Large caps perform during stability

- Mid & small caps outperform during growth phases

- Debt provides cushion during volatility

- You participate in multiple growth opportunities

- Your downside is limited during corrections

- Your portfolio remains resilient across market cycles

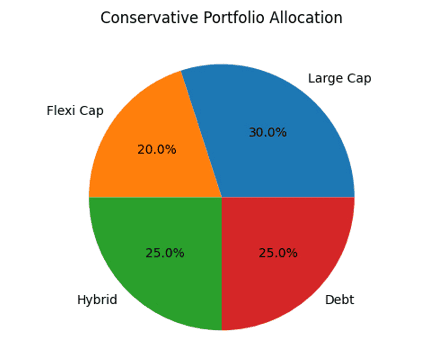

Allocation Breakdown:

- Large Cap Fund – 30%

- Flexi Cap Fund – 20%

- Hybrid Fund – 25%

- Debt Fund – 25%

What Makes It Effective?

- Large caps provide stability

- Hybrid & debt reduce volatility

- Flexi cap adds moderate growth

Ideal For:

- First-time investors

- Retirees

- Low-risk appetite individuals

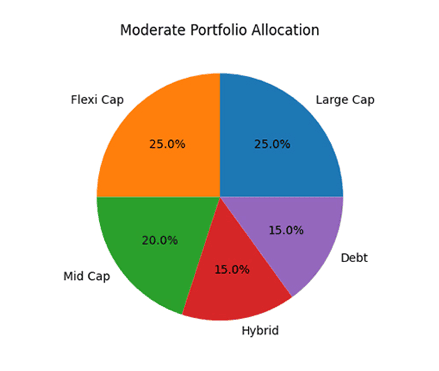

Allocation Breakdown:

- Large Cap – 25%

- Flexi Cap – 25%

- Mid Cap – 20%

- Hybrid – 15%

- Debt – 15%

Why This Works

- This is the sweet spot portfolio:

- Growth + Stability

- Risk is controlled but not avoided

- Suitable for most investors

Ideal For:

- Salaried professionals

- Long-term wealth creators

- Investors with medium risk appetite

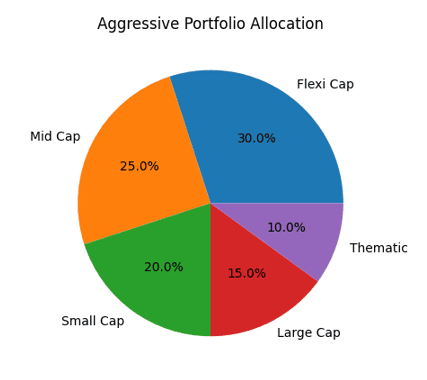

Aggressive Portfolio (Growth Maximization)

Allocation Breakdown:

- Flexi Cap – 30%

- Mid Cap – 25%

- Small Cap – 20%

- Large Cap – 15%

- Thematic – 10%

- High volatility in short term

- Strong wealth creation in long term

- Requires patience & discipline

- Young investors

- Long-term goals (10+ years)

Lumpsum vs SIP: The Smart Approach

Many investors also struggle with timing:

Should you invest ₹10 lakh at once?

Better Strategy: STP (Systematic Transfer Plan)

- Park funds in a liquid fund

- Transfer gradually over 3–6 months

- Reduce timing risk

- Benefit from market fluctuations

This approach combines the power of lumpsum + safety of SIP

Common Mistakes to Avoid

- Investing in too many funds (over-diversification)

- Chasing past performance

- Ignoring asset allocation

- Panic selling during market corrections

The Final Verdict

- One fund = Simple but risky

- Multiple funds = Balanced and strategic

The winner is not “more funds” but “right allocation.”

A well-structured portfolio:

- Protects during downturns

- Grows during upcycles

- Delivers consistent long-term wealth

Closing Thought

“Wealth is not created by timing the market, but by time in the market—with the right strategy."

Disclaimer

Mutual fund investments are subject to market risks. Read all scheme-related documents carefully before investing. Past performance is not indicative of future returns. The above portfolios are illustrative and should be customized based on individual financial goals and risk appetite.